How Mortgage Rates Follow Treasury Yields

Fixed Mortgage Rates Vs. Treasury Yields

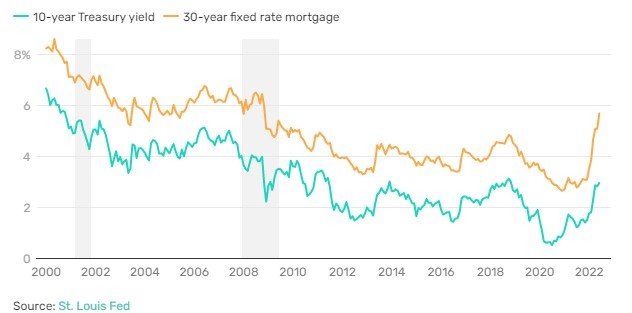

It may interest you to note that the relationship between 10-Year Treasury notes and mortgage rates is surprisingly intertwined. While it’s true that many factors can impact the growth or decline of interest rates (like government policy, economic reality, etc.), knowing how 10-year Treasury yields affect the rise or fall of mortgage rates can prove helpful. That’s because as yield curves change on 10-Year Treasury bonds and notes, they can also influence mortgage rates (and monthly mortgage payments) in turn.

Fixed mortgage rates dropped to historic lows in 2020 as a result of the Federal Reserve lowering the target for the fed funds rate to virtually zero on March 15, 2020. The Fed's interest rate cuts were in response to the COVID-19 pandemic and the resulting recession.

Investors fled to the safety of government securities pushing yields on the 10-year Treasury note to an all-time low of 0.52% on Aug. 4, 2020. As a result, mortgage rates fell since they tend to follow the yields on U.S. Treasury notes.

However, by 2022, the Fed was hiking rates to combat inflation, and by May of 2022, the 10-year Treasury yield had risen to nearly 3.5%, pushing mortgage rates to over 5%.

When there's not much demand, bond (treasury) prices drop, and yields increase to compensate. That makes it more expensive to buy a home. And when buyers have to pay more for their mortgage, they are forced to buy less expensive homes, which encourages builders and sellers to lower home prices.

Treasury notes, bonds, and bills all have an impact on current mortgage rates for homeowners. Moreover, the higher that Treasury yields go, the higher that mortgage interest rates tend to climb and vice versa.